How Much Money Do I Need To Live Well

How much money do you need to comfortably retire? $1 1000000? $2 one thousand thousand? More than?

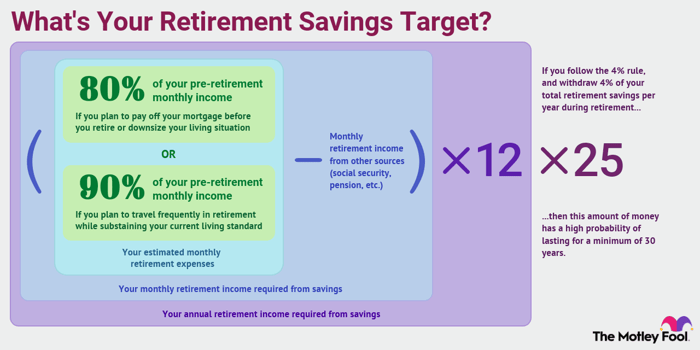

Financial planners often recommend replacing well-nigh 80% of your pre-retirement income to sustain the same lifestyle later yous retire. That means if y'all earn $100,000 per year, yous'd aim for at least $80,000 of income (in today's dollars) in retirement.

Nevertheless, there are several factors to consider, and non all of this income will demand to come from your savings. With that in mind, here'due south a guide to aid summate how much money you will demand to retire.

It's not about money, information technology's about income

Ane important signal when information technology comes to determining your retirement "number" is that it isn't nigh deciding on a certain amount of savings. For instance, the most mutual retirement goal among Americans is a $1 million nest egg. Merely this is faulty logic.

Image source: Getty Images.

The most important factor in determining how much yous need to retire is whether yous'll have plenty money to create the income y'all need to support your desired quality of life after you retire. Will a $i one thousand thousand savings balance permit you lot to create enough income forever? Perhaps, only maybe not. That's what we're going to determine in this article.

So how much income practise you demand?

The reason y'all don't demand to replace 100% of your pre-retirement income is that when you retire, y'all're typically able to eliminate certain expenses. For example:

- You lot'll no longer have to save for retirement (obviously).

- Yous might spend less on commuting expenses and other costs related to going to work.

- You may have paid off your mortgage by the fourth dimension you lot retire.

- You may not demand life insurance if yous no longer have dependents.

Only retiring on 80% of your almanac income isn't perfect for anybody. You might desire to accommodate your goal up or down based on the type of retirement lifestyle you plan to have and if your expenses will exist significantly different.

For example, if you programme to travel frequently in retirement, yous may desire to aim for 90% to 100% of your pre-retirement income. On the other manus, if you plan to pay off your mortgage earlier you retire or downsize your living situation, you lot may be able to alive comfortably on less than 80%.

Let's say yous consider yourself the typical retiree. Between yous and your spouse, you lot currently have an annual income of $120,000. Based on the 80% principle, you can await to demand nigh $96,000 in annual income after yous retire, which is $viii,000 per month.

Social Security, pensions, and other reliable income sources

The good news is that, if you're like most people, y'all'll get some help from sources other than your savings, such as your Social Security benefits. For most people, Social Security is a significant income source.

But the percentage of income that Social Security will replace is typically lower for college-income retirees. For case, Allegiance estimates that someone earning $fifty,000 a year can expect Social Security to supersede 35% of their income. But someone earning $300,000 a twelvemonth would have a Social Security income replacement rate of only 11% on average.

If you lot aren't sure how much you tin can wait, check your latest Social Security statement, or create a my Social Security account to get a skillful estimate based on your work history.

If you lot have any pensions from electric current or former jobs, be sure to have those into consideration. The same goes for any other predictable and permanent sources of income -- for example, if you bought an annuity that kicks in after you retire.

Continuing our instance of a couple that needs $8,000 in monthly income to retire, let'southward say each spouse is expecting $1,500 per month from Social Security, and that one spouse also has a $1,000 monthly pension. This means that, of the $viii,000 in monthly income needs, $four,000 is being taken care of past sources other than savings.

So, in summary, you can estimate the monthly retirement income you need to generate using this formula:

Monthly income required = Estimated monthly retirement expenses-Monthly retirement income from other sources

How much savings will you lot demand to retire?

Now allow'south determine how much savings you'll need to retire. After you've figured out how much income yous'll need to generate from your savings, the next step is to calculate how big your retirement nest egg needs to be for yous to produce this much income in perpetuity.

A retirement calculator is ane option. Or, y'all can use the "4% rule." The iv% dominion says that in your first twelvemonth of retirement, you can withdraw iv% of your retirement savings.

So, if you take $one million saved, you would have $forty,000 out during your first year of retirement either in a lump sum or as a series of payments. In subsequent years of retirement, you would adjust this amount upward to go on up with cost-of-living increases.

The well-nigh important consideration in deciding how much you lot need to retire is whether you'll accept plenty money to create the income y'all need to support your desired quality of life afterward you retire.

The idea is that if you follow this rule, you lot shouldn't take to worry about running out of money in retirement. Specifically, the 4% rule is designed to make sure your money has a high probability of lasting for a minimum of 30 years.

To calculate a retirement savings target based on the iv% rule, yous apply the following formula:

Retirement savings target = Annual income required 10 25

Continuing our case, we saw in the previous section that our couple would need $iv,000 per month ($48,000 per year) from their savings. So, in this example, our couple should aim for $1.2 one thousand thousand in retirement savings accounts, such every bit a 401(k) plan or private retirement account (IRA), to provide $48,000 per yr in sustainable retirement income.

It's of import to note that the iv% rule has a number of flaws. Information technology assumes you'll withdraw the aforementioned corporeality each yr in retirement, adjusted for inflation. Information technology also assumes your portfolio volition be split between stocks and bonds throughout your retirement.

The bottom line on retirement savings goals

At that place is no perfect method of calculating your retirement savings target. Investment operation will vary over time, and it can be difficult to accurately project your actual income needs.

Furthermore, it'south worth mentioning that not all retirement plans are equal when it comes to income. Money you withdraw from a traditional IRA or 401(k) will be considered taxable income. On the other paw, any coin you withdraw from a Roth IRA or Roth 401(chiliad) is generally not taxable at all, which may alter the calculation a chip.

At that place are other potential considerations likewise. Many workers accept to retire before than they planned. For instance, most three 1000000 workers retired before than they predictable because of the COVID-19 pandemic. Even in normal times, older workers oft have to retire early due to layoffs, wellness problems, or caregiving duties. Saving for a longer retirement than anticipated gives you a rubber cushion.

Information technology'due south likewise important to consider the bear upon of inflation on your retirement plans. Inflation has gotten a lot of attention in 2022 every bit prices accept increased at the fastest stride we've seen in 40 years. But fifty-fifty when costs rise at a typical charge per unit, inflation hits senior households harder than working-age households. That's because seniors spend a higher portion of their incomes on expenses such as healthcare and housing, which tend to increment faster than the overall inflation rate.

While nosotros're trying to present the broad strokes here, it's still a good idea to consult a financial advisor who can not only tailor a retirement savings goal to your item situation but tin can as well assist set you on the right path with a savings and investment program that can make certain you reach your goals.

By using the methods discussed in this article, you can get a adept idea of how much you'll need to salvage to retire comfortably. Continue in mind this isn't designed to exist a perfect method only a starting indicate to help you appraise where you are and what adjustments you lot might need to make to go where yous need to be.

Expert Q&A

The Motley Fool caught upwardly with retirement skilful David John, a senior strategic policy advisor at the AARP Public Policy Constitute.

David C. John, MA, MBA, AARP Senior Policy Counselor. David's areas of focus are retirement savings, pensions, annuities, international pension and retirement savings systems, and Alimony Benefit Guaranty Corporation (PBGC).

The Motley Fool: What is your communication for someone who may be worried about retiring because of contempo financial setbacks?

David John: If your health, family responsibilities, and task status allows, continue to work longer than you might take before. The extra time allows yous to salve more and for the markets to continue to recover from past losses. Most important, delay taking your Social Security for every bit long every bit possible then you lot'll have a larger, inflation-protected benefit.

The Motley Fool: There are no difficult and fast rules about when to retire or how much nosotros should have saved, but what three pieces of advice would you requite someone who is just starting their showtime retirement savings business relationship?

David John:

- Make saving a priority and contribute a consistent percentage of your income that grows over fourth dimension every payday.

- Invest only in a diversified option like a target date fund that uses passive index funds. Don't endeavour to crush the market place with your retirement money.

- Don't have a withdrawal unless you absolutely have to. Instead, starting time a divide emergency fund in addition to your retirement account.

Source: https://www.fool.com/retirement/how-much-do-i-need/

Posted by: pelletiermoseeld.blogspot.com

0 Response to "How Much Money Do I Need To Live Well"

Post a Comment